This is the best way to present your PowerPoint over Teams while being able to see the presenter notes.

On the Slide Show tab in the ribbon, click the “From Beginning” button. This will take your presentation full screen.

Use Alt-Tab (Cmd-Tab on a Mac) to cycle through the open applications and select the Teams meeting window.

Click the sharing button in Teams and choose the PowerPoint that is in full screen presentation mode.

Use Alt-Tab (Cmd-Tab on a Mac) to cycle back to your presentation

Right click on the presentation and choose “Use Presenter View”.

The people in the Teams meeting will see the presentation. They won’t see the presenter’s notes. This will give you the best set up for conducting the presentation while giving the audience your slides at full size.

Teams has a built in option to share a PowerPoint but this uses PowerPoint for the web. This has a limited feature set so some of your animations or transitions may not work as intended. The other downside is that you can’t see your presenter’s notes.

The Canada Emergency Business Account (CEBA) requirements and deadlines have changed.

As of December 4, 2020, CEBA loans for eligible businesses will increase from $40,000 to $60,000.

Applicants who have received the $40,000 CEBA loan may apply for the $20,000 expansion, which provides eligible businesses with an additional $20,000 in financing.

All applicants have until March 31, 2021, to apply for $60,000 CEBA loan or the $20,000 expansion.

The government has announced three key changes to the Canada Emergency Business Account (CEBA) program.

As of October 26, 2020, eligible Canadian businesses that currently operate through a personal bank account will be able to apply for CEBA.

All applicants now have until December 31, 2020, to apply for CEBA.

COMING SOON -CEBA support is being expanded from $40K to $60K. This expansion will be available to all eligible previous and new CEBA applicants. An announcement with further details will be made in coming weeks.

If you have not yet applied for CEBA or were turned down because you operate your business out of a personal account, now is the time to apply.

The first step would be to complete the online CEBA pre-screening tool to see if you are eligible. Your financial institution will likely ask for the results of this assessment when you apply so it should be your first stop in the application process.

The Canada Emergency Wage Subsidy (CEWS) is a subsidy that generally covers 75% of an employee’s wages – up to $847 per week - for employers of all sizes and across all sectors who have suffered a drop in gross revenues of at least 15% in March, and 30% in April and May.

The program will be in place for a 12-week period, from March 15 to June 6, 2020.

Employers who are eligible for the CEWS are entitled to receive a 100% refund for certain employer contributions to Employment Insurance, the Canada Pension Plan, the Quebec Pension Plan, and the Quebec Parental Insurance Plan paid in respect of employees who are on leave with pay.

For employers that are eligible for both the CEWS and the 10% Temporary Wage Subsidy for a period, any benefit from the Temporary 10% Wage Subsidy for remuneration paid in a specific period will generally reduce the amount available to be claimed under the CEWS in that same period.

Eligible Employers

To qualify you must:

be an eligible employer

have experienced an eligible reduction in revenue, and

have had a CRA payroll account on March 15, 2020

Types of Eligible Employers

individuals (including trusts)

taxable corporations

persons that are exempt from corporate tax (Part I of the Income Tax Act), other than public institutions:

non-profit organizations

agricultural organizations

boards of trade

chambers of commerce

non-profit corporations for scientific research and experimental development

labour organizations or societies

benevolent or fraternal benefit societies or orders

registered charities

partnerships consisting of eligible employers

Ineligible Employers

Public institutions including:

municipalities and local governments

Crown corporations

public universities

colleges

schools

hospitals

Eligible Revenue Reduction

You must determine if your reduced revenue makes you eligible to apply for the wage subsidy in a particular period.

Eligible revenue generally includes revenue earned in Canada from:

selling goods

rendering services, and

others' use of your resources

Use your normal accounting method when calculating revenue. You can use the cash method or the accrual method, but you must use the same approach throughout.

If you determine that you qualify for the CEWS for one claim period, you will automatically qualify for the following claim period.

Calculate your reduction by comparing your eligible revenue for the starting month of the claim period with your baseline revenue. Your baseline revenue is either:

the revenue you earned in the corresponding month in 2019, or

the average of the revenue you earned in January and February, 2020

You must choose one of these baseline revenue options for your method of comparison and will not be able to change it for your subsequent calculations for the other 2 periods.

Period Dates

Baseline Revenue

Eligibility Period Revenue

Required Reduction

March 15, 2020 to April 11, 2020

March 2019, or an average of January and February 2020

March 2020

15%

April 12, 2020 to May 9, 2020

April 2019, or an average of January and February 2020

April 2020

30%

May 10, 2020 to June 6, 2020

May 2019, or an average of January and February 2020

May 2020

30%

Eligible Employees

When applying for CEWS or calculating the amount of wage subsidy to expect, you will need to understand which of your employees are eligible to be included in the calculation. You will also need to know the amount of their pay (eligible remuneration).

Who Are Eligible Employees

An eligible employee is an individual employed in Canada by you (the eligible employer) during the claim period, except if there was a period of 14 or more consecutive days in that period in respect of which they were not paid eligible remuneration by you.

Employee eligibility is based on whether the person is employed in Canada, not where they live.

Retroactively Hiring and Paying Employees

Employees who have been laid off or furloughed can become eligible retroactively, as long as you rehire them and their retroactive pay and status meet the eligibility criteria for the claim period. You must rehire and pay such employees before you include them in your calculation for the subsidy.

What Is Eligible Remuneration

Eligible remuneration includes amounts you paid an employee as salary, wages and other taxable benefits, fees, and commissions. These are amounts employers would be required to make payroll deductions on to be remitted to the CRA.

Severance pay and items such as stock option benefits or the personal use of a corporate vehicle are not part of eligible remuneration.

Baseline Remuneration

When calculating the wage subsidy, you will need to determine an employee’s baseline remuneration. Baseline remuneration is considered to be the average weekly eligible remuneration paid to an employee during the period of January 1, 2020, to March 15, 2020. However, you may exclude from your calculation any period of seven or more consecutive days in respect of which the employee was not paid.

Application Process

If you are applying for CEWS yourself the best way to apply is through My Business Account on the CRA website. If you are not set up for My Business Account with CRA, it’s a good idea to get set up. The government will likely administer other programs using this site. Also, remember to register your bank account for pre-authorized deposits from CRA so that you get your money quicker.

This $25 billion program provides interest-free loans of up to $40,000 to small businesses and not-for-profits, to help cover their operating costs during a period where their revenues have been temporarily reduced, due to the economic impacts of the COVID-19 virus.

Eligibility Requirements

The Borrower is a Canadian operating business in operation as of March 1, 2020.

The Borrower has a federal tax registration.(See our post for an explanation of Business Numbers)

The Borrower’s total employment income paid in the 2019 calendar year was between Cdn.$20,000 and Cdn.$1,500,000. This can be found from your T4 Summary (T4SUM). A copy of this is available in the Canada Revenue Agency’s (CRA) My Business Account service.

The Borrower has an active business chequing/operating account with the Lender, which is its primary financial institution. This account was opened on or prior to March 1, 2020 and was not in arrears on existing borrowing facilities, if applicable, with the Lender by 90 days or more as at March 1, 2020. You should apply at the financial institution where your main chequing account is located.

The Borrower has not previously used the Program and will not apply for support under the Program at any other financial institution. These are government loans and they will check their records to make sure you’ve applied only once.

The Borrower acknowledges its intention to continue to operate its business or to resume operations.

The Borrower agrees to participate in post-funding surveys conducted by the Government of Canada or any of its agents.

Ineligible Borrowers

It is not a government organization or body, or an entity owned by a government organization or body;

It is not a union, charitable, religious or fraternal organization or entity owned by such an organization or if it is, it is a registered T2 or T3010 corporation that generates a portion of its revenue from the sales of goods or services;

It is not an entity owned by individual(s) holding political office; and

It does not promote violence, incite hatred or discriminate on the basis of sex, gender, sexual orientation, race, ethnicity, religion, culture, region, education, age or mental or physical disability.

Use of Funds

The funds from this loan shall only be used by the Borrower to pay non-deferrable operating expenses of the Borrower including, without limitation, payroll, rent, utilities, insurance, property tax and regularly scheduled debt service, and may not be used to fund any payments or expenses such as prepayment/refinancing of existing indebtedness, payments of dividends, distributions and increases in management compensation.

This means that the funds must be used for normal cash flow purposes. You can’t pay down a lump sum on other debt or pay yourself a dividend from these funds.

If you qualify, this is a program worth participating in. During times like these, you’ll want to keep as much cash on hand as possible. Remember, this is an interest free loan. Also, repaying the balance of the loan on or before December 31, 2022 will result in loan forgiveness of 25 percent (up to $10,000). If you can’t repay the loan by the end of 2022, your lender will convert the loan into a regular term loan with payments.

The Saskatchewan government has announced the Saskatchewan Small Business Emergency Payment Program. It’s a program meant to help out businesses that have had a loss in revenue due to a COVID-19 public health order. If your business hasn’t been ordered to close or modify your operations due to a public health order, you won’t be eligible for this program.

Benefits

Payments are based on 15% of a business’s monthly sales revenue in either April 2019 or February 2020. Businesses may select either of these months to calculate their payment so pick the month that gives you the highest payment.

The maximum payment is $5,000 per business.

The funds can be used for any purpose, including paying fixed costs or expenditures related to re-opening the business following the pandemic.

Eligibility

Have been carrying on business in Saskatchewan on February 29, 2020;

Have been ordered to temporarily close or curtail operations through a COVID-19 public health order;

Have less than 500 employees;

Attest that they:

have experienced a loss in revenue due to a COVID-19 public health order;

plan to reopen operations following the cancellation of the COVID-19 public health order; and

have not received any payments or amounts from any other sources, including insurance, to replace or compensate for the loss of sales revenue other than amounts from other government assistance programs; and

Apply on or before July 31, 2020.

How to Apply

You will need to complete the application on the government’s website. If you qualify for this program, you should apply. No one knows how long the public health order will last and you will want to have as much cash on hand as possible.

I’ve learned over the years that people can often be confused about the purpose of a business plan. Some see it as a means to an end — a necessary prerequisite for getting a loan from a banker or to satisfy the obligations for a commercial real estate lease.

The biggest value of a business plan is the planning and thought that goes into its creation. The tweet below from @WilHarris illustrates this nicely.

Great way of framing startup biz planning, too. You’re start-up will never stick to the biz plan, but the act of planning and scenario scoping is invaluable. 📈 https://t.co/PfKki21Fng

Wil is talking about early stage start-ups that don’t have a well defined business model and are trying to find product/market fit. Those types of businesses will change significantly between inception and profitability.

However, the same holds true for more traditional businesses with proven business models. The amount of change in the business and deviation from the business plan are reduced but the actual execution of the business will still not match the plan exactly.

Part of the reason for this is that assumptions made during the business planning process may turn out to be just plain wrong. There are a lot of variables to consider when drafting a business plan. Not all of them will be estimated correctly.

Changing conditions and new information will have an impact on the development of a business. If you think of a business plan as a roadmap that you are using to go on a long journey, issues may present themselves that cause you to take an alternate route. A bridge could be washed out or a rock slide could be blocking the highway.

The same thing happens in business. You may get to a certain point with your business and then need to make a change due to new information or changing conditions. Maybe the product you thought would be your big seller isn’t and you need to focus on another product line. Perhaps foot traffic to your store isn’t what you thought it would be and so you need to rely more on sales through your website.

This is all fine and it is to be expected. A business plan should be a living document that is updated to reflect changing conditions and new information. The value is in the planning and the analysis of different possible scenarios and their impact on the business.

Taking the time to evaluate what impact a decision will have on the financial performance of your business can mean the difference between the business thriving or needing to it shut down. The time and money you will spend creating a business plan and keeping it up to date will be well worth the investment.

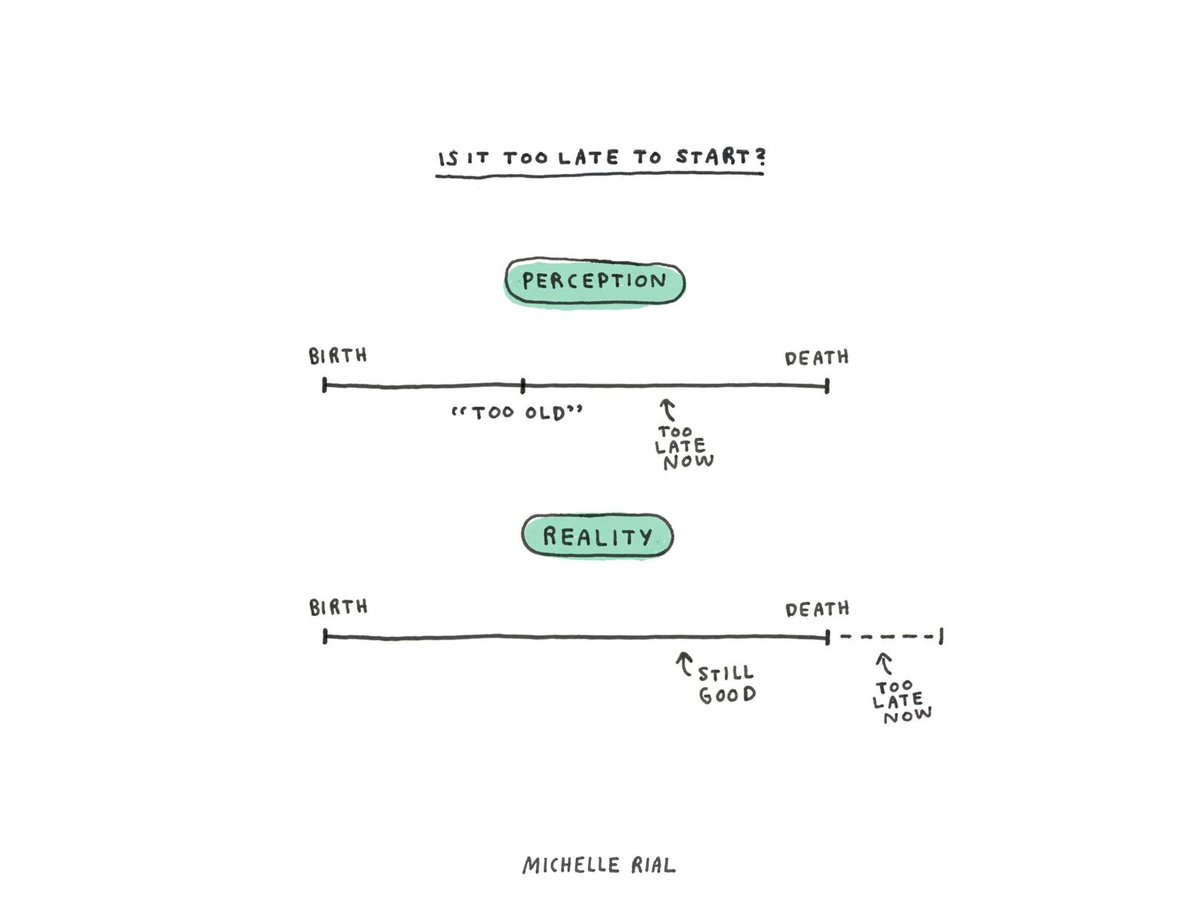

We’ve just entered into another New Year and it is a natural point for people to reflect on the year past and what lies ahead. If you have had starting a business on your mind for a few years now, you might be thinking, “Have I missed my window of opportunity for this?” “Is it too late to pursue my dream of starting a business?” Fortunately, the answer is no.

This illustration from Michelle Rial’s book, Am I Overthinking This?, demonstrates this wonderfully.

Entrepreneur Gary Vaynerchuk has a very similar outlook.

Before you write this off as a couple of people just being overly optimistic, you should know that there is research that backs up the idea that businesses started by older entrepreneurs are more successful.

A research article in Harvard Business Review1 found that the average age of an entrepreneur when starting a business is 42. Even when filtering the data to analyze just the founders of software startups, the average age is 40. It seems that the young software startup founders are just the ones that you hear about the most.

The same study found that the top 0.1% of startups, based on their growth rates during their first 5 years of business, were started by people who were on average 45 years old. The authors state that:

“If you were faced with two entrepreneurs and knew nothing about them besides their age, you would do better, on average, betting on the older one.”

Why is this? Experience matters. Reading books and attending university classes are valuable but some things can only be learned through real world experience. Someone with 20 years of experience in an industry is going to have a very good foundation on which to start a business.

The idea that starting businesses is only for the young is simply a myth. If you have what it takes to be an entrepreneur, don’t let age stand in your way.

Azoulay, P., B. Jones, J. D. Kin, and J. Miranda. “Research: The average age of a successful startup founder is 45.” Harvard Business Review (2018). ↩︎

PayPal Canada, Facebook Canada and BDC are joining AmberMac Media and Pint Glass Productions to launch HerTurn, Canada’s new online business competition series for women entrepreneurs.

The competition will take applications over a six week period. Three finalists will be chosen from the list of applicants and they will participate in a series of challenges with the competition’s mentors. A winner will be chosen based on the outcome of the challenges and will receive a grand prize valued at $20,000 worth of cash and prizes thanks to PayPal Canada, which includes $15,000 CAD and $5,000 worth of marketing services from AmberMac Media Inc.

The competition launches September 16th and applications are open through to October 28, 2019. A winner will be chosen by December 15, 2019. This could be a good opportunity for you to get exposure for your business as well as to learn marketing from one of the best in the business.

The Canadian Competition Bureau has put out a call-out for information. The Bureau is looking into concerns that online search, social media, display advertising and online marketplaces, have become increasingly concentrated, to the detriment of consumers and businesses.

As the multi-national companies start to find that growing revenue is becoming more difficult, they are starting to try new strategies and tactics to make money. Some of these aren’t always in the best interest of entrepreneurs with small businesses. Increasingly, entrepreneurs are having to pay to have visibility in markets that previously would have been available to them for free. This is a problem as many small businesses and new businesses don’t have the resources to buy this access.

It’s incredibly important that access to the Internet and the ability to be found by potential customers have a very low barrier to entry. Any Canadian entrepreneur willing to put in the effort and build the skill to create an online business, should be able to do so at minimal cost. This will ensure that this opportunity is available to the largest group of people.

If you have been negatively affected by a lack of competition in digital markets or if you have concerns about too much power being in too few hands, you can make an anonymous submission to the Bureau. The deadline for submissions is November 30, 2019.